Self-Employed and Employed in Germany 2026: Taxes for Side Hustlers

Full-time job plus a side business in Germany — how the tax office combines both incomes in 2026, what you have to file, and how to avoid back-payment surprises.

- Category

- Taxes

- Updated

- Author

- Diana

You mastered taxes for your day job — then started a side business and suddenly you're juggling two worlds at once: payroll tax from your employment and income tax from your self-employment. What most people underestimate: the tax office merges both incomes at the end of the year — and that's where the biggest surprise bills come from. Here's what you need to know in 2026 to keep your second income from becoming a tax trap.

Key points at a glance

- Both incomes are added together. Salary (Anlage N) and side-business profit (Anlage S or G) combine into your taxable income — the tax office applies your personal rate to that total.

- Härteausgleich up to €820: profit up to €410 is tax-free, between €410 and €820 only part is taxed, above €820 it's fully taxable.

- Filing duty from €410 profit from self-employment — even though your day job is already settled via payroll.

- Trade tax only above €24,500 profit, Kleinunternehmer turnover limit €25,000 (prior year) / €100,000 (current year).

- Build a reserve: set aside 30–40 % of every euro of side-business profit — the back-pay plus retroactive prepayments often hit together with your first assessment.

Two income types — how the tax office combines them

Your gross salary goes on Anlage N. Your self-employment profit lands on Anlage S (Freiberufler) or Anlage G (Gewerbetreibender). The tax office calculates your personal tax rate on the sum of both incomes — and with a full-time salary in the background, that rate is often 30–42 %, much higher than if your €5,000 freelance profit were taxed alone. That's why "just doing a small EÜR" isn't enough.

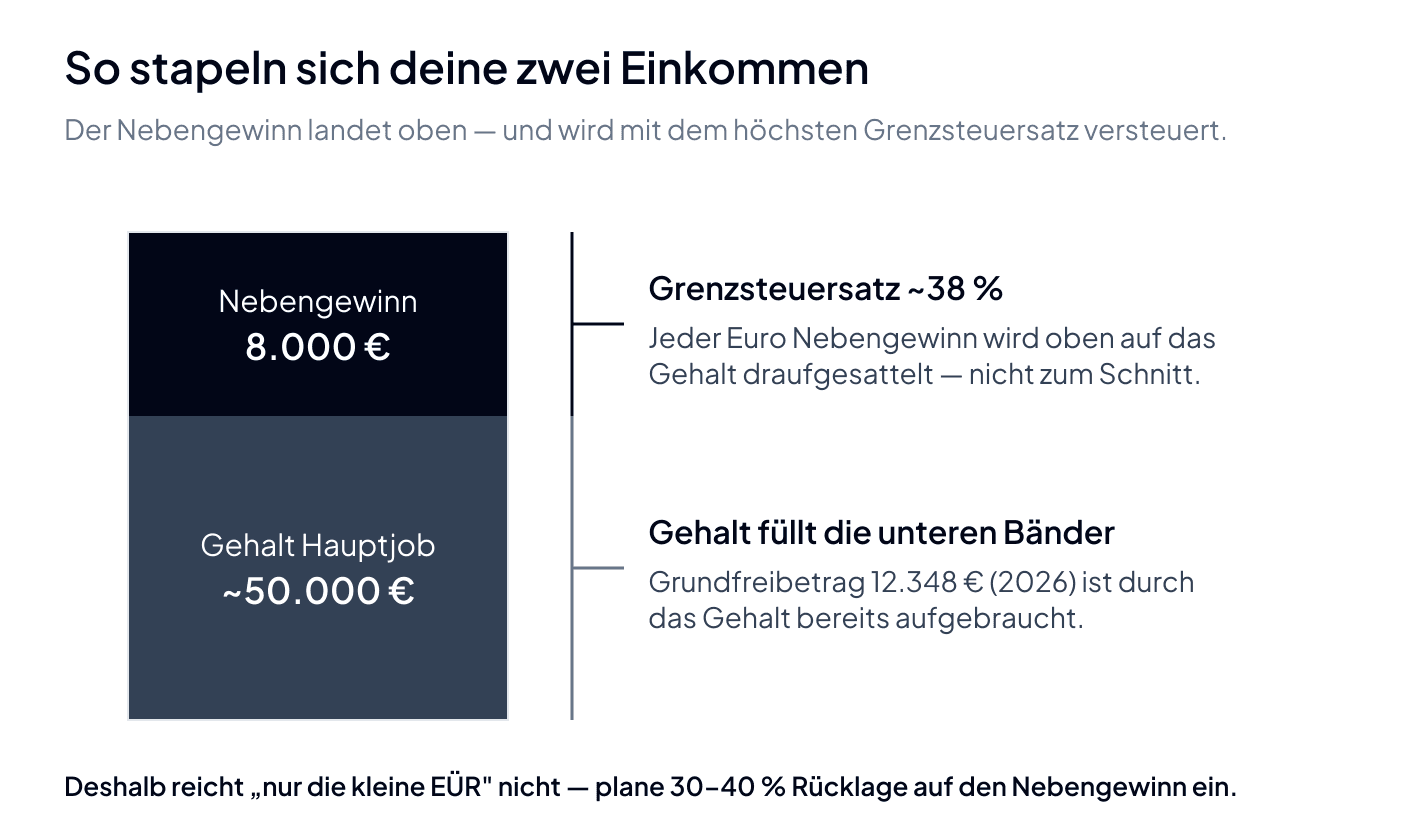

The effect is called progression: every euro of side-business profit is taxed "on top of" your salary — at your marginal rate, not your average rate. On a gross salary of around €50,000, that marginal rate already sits near 38 %. The basic tax-free allowance of €12,348 (2026) is long used up by your salary — so it doesn't shield your side income a second time.

| Income | Form | Tax effect |

|---|---|---|

| Gross salary (day job) | Anlage N | Payroll tax already withheld, €1,230 lump sum applied automatically |

| Freelance profit | Anlage S + EÜR | Fully taxed at your marginal rate |

| Trade-business profit | Anlage G + EÜR | Income tax + trade tax above €24,500 |

| Taxable income | Sum | Personal rate on the whole |

The €410 threshold and Härteausgleich

Section 46(3) of the Einkommensteuergesetz defines two thresholds. Secondary income up to €410 per year is tax-free. Between €410 and €820, the Härteausgleich kicks in — you only tax a partial amount, calculated as (2 × secondary income − €820). Above €820 profit, the side business is fully taxable. Important: the thresholds apply to income, i.e. revenue minus business expenses — not turnover. Take in €700 with €350 in expenses and your €350 of income stays entirely tax-free.

| Side-business profit per year | Taxable share | Example |

|---|---|---|

| up to €410 | €0 | €400 profit → €0 taxed |

| €410 – €820 | 2 × profit − €820 | €600 profit → €380 taxed, €220 free |

| from €820 | full profit | €900 profit → €900 taxed |

The Härteausgleich is genuine relief — but only for tiny side incomes. Once your self-employment is running seriously, the whole profit is in. The tax office applies the adjustment automatically; you don't have to request it.

Which taxes actually apply?

Three tax types can land on your side activity — but rarely all at once. This overview shows when each applies:

| Tax | Who pays | Threshold / allowance |

|---|---|---|

| Income tax | anyone with profit above the Härteausgleich | fully from €820 profit, basic allowance €12,348 used up by salary |

| VAT | anyone not a Kleinunternehmer | over €25,000 turnover (prior year) / €100,000 (current year) |

| Trade tax | only Gewerbe, not freelancers | allowance of €24,500 profit per year |

For most side hustlers it stays with income tax: freelancers never pay trade tax, and below €24,500 profit a side trade business doesn't either. For VAT, only your turnover matters, not your day-job salary.

Anlage N, S, G and the EÜR — what you actually file

Once taxable, you submit an annual income tax return with the relevant appendices — even though your day job is already settled via payroll. The filing duty for the self-employment already starts at €410 profit. That return usually includes an Einnahmenüberschussrechnung (EÜR) as a separate form. Freelancers add Anlage S, trade businesses Anlage G. Your employment income stays on Anlage N — both forms coexist in the same return. How to declare a part-time self-employment to your health insurer and employer is a separate topic in itself.

The starter book for your self-employment

Free e-book: registration, accounting, your first invoice, and taxes — plus a tax calendar, deductions cheat sheet, and invoice template.

VAT — Kleinunternehmer or standard?

Regardless of your job, your self-employment has its own VAT profile. If your revenue is under €25,000 in the prior year and €100,000 in the current year (thresholds updated in 2025), you can choose the Kleinunternehmerregelung — no VAT on invoices, no VAT preliminary returns. Once you exceed those limits, you're subject to standard VAT: charge it on invoices and file quarterly (sometimes monthly) returns. The Kleinunternehmer scheme stays open to you even if your day job pays well — it depends only on your self-employment turnover, not your total income.

Prepayments — the trap after your first tax bill

Classic stumbling block: in your first year of side-business activity, you pay no income tax prepayments because the tax office hasn't acted on your tax registration questionnaire yet. Your first tax assessment hits with the back-pay — and at the same time, the tax office retroactively sets prepayments for the current and next year. Worst case, you owe four quarters on the same day. From euro one of profit, set aside 30–40 % as a tax reserve.

Worked example: what's left of €8,000 side profit

Take an employee earning around €50,000 gross who makes €8,000 profit on the side and stays under the Kleinunternehmer limit as a freelancer. Here's the rough math:

| Item | Amount |

|---|---|

| Side profit (revenue − business expenses) | €8,000 |

| Personal marginal rate (day job ~€50,000) | ~38 % |

| Income tax (plus Soli if applicable) on the side profit | approx. €3,040 |

| Trade tax (freelancer, none anyway) | €0 |

| VAT (Kleinunternehmer) | €0 |

| = Net from the side activity | approx. €4,960 |

| Recommended tax reserve (35–40 %) | ~€2,800–3,200 |

The figures are illustrative — your exact marginal rate depends on salary, tax class and deductions. The message holds: about a third of every euro of side profit belongs to the tax office. Don't set it aside and you'll fund the back-payment out of your salary.

Health insurance and pension — what changes

If you're publicly insured through your day job, you generally stay covered — the side business is considered "secondary." The key test: your hours and income from the side must stay below your main job. Earn more or work more on the side, and the self-employment becomes your primary occupation — meaning you pay the full health and pension contributions yourself, easily €300–400/month more. For pension insurance, some professions (artists, caregivers, teachers) face mandatory contributions even part-time.

The health insurer tests "secondary" status on two criteria: time and money. If both stay below your main job, your contribution doesn't change. If one tips over for good, the insurer reclassifies you — best to raise it with them proactively before they do it retroactively.

Hourly rate and expense rules — separate both worlds cleanly

For the side business to actually pay off, your hourly rate has to cover taxes, social charges, and reserves — or you'll net less than your day-job hour. Also important: Werbungskosten (employee expenses) and Betriebsausgaben (business expenses) go on different forms. The €1,230 employee lump sum is deducted automatically on Anlage N; your self-employment business expenses go separately into the EÜR. A laptop you use both for your job and your business has to be allocated pro rata — cleanest to claim it 100 % as a business expense and tax the private use.

There's a lot of advice on when to leave employment and focus fully on self-employment. Some recommend waiting until your self-employment income reaches 80 % of your salary, others until it's above 120 % for three months or more. In my experience, the most important thing is to feel that the income is stable and not a one-off.

Peter BoykoFounder of Norman

Peter BoykoFounder of NormanBookkeeping on top of your day job — the easy fix

Nobody wants to fight Excel after a full day at work. Norman handles it automatically: photograph receipts, AI categorizes them under SKR03/04, EÜR and Anlage S/G generate at the touch of a button, tax workflows for the self-employed run straight to ELSTER. That saves two to three hours per month — and is worthwhile even below €25,000 in revenue, because you stop accumulating receipts in a drawer.

Frequently asked questions

From what profit do I have to file a tax return?

Once your self-employment profit exceeds €410 a year, you're obliged to file an income tax return — with Anlage S or G plus the EÜR, on top of Anlage N for your day job. Below €410, the Härteausgleich applies and no tax arises on the side income.

Do I have to tell my employer about my side business?

Legally you need no approval — freedom of occupation (Art. 12 of the Basic Law) allows side activities. But many employment contracts include a notification or approval clause. A side business is permitted as long as it doesn't compete with your employer and doesn't impair your work performance. Transparency is usually the safer route.

Do I pay trade tax on my side income?

As a freelancer, never. As a trade business, only once your trade profit exceeds €24,500 a year — until then the trade-tax allowance protects you. Trade tax paid is also largely credited against your income tax.

Does my side income stay tax-free under €410?

Yes, provided it's your only secondary income and you also draw employment wages. What counts is profit (revenue minus expenses), not turnover. Between €410 and €820 only part is taxed; above that, the full profit.

Can I use the Kleinunternehmer scheme even though I'm employed?

Yes. The Kleinunternehmer scheme depends only on your self-employment turnover (under €25,000 in the prior year, €100,000 in the current year) — your day-job salary doesn't count. You skip VAT on invoices and the VAT preliminary returns.

When does my self-employment become my main occupation?

When you permanently earn more or work more hours in the self-employment than in your day job. The health insurer then reclassifies you, and you pay health and long-term care contributions in full yourself — often €300–400/month more than your previous employee share.

Conclusion

Running a side business while employed in Germany is tax-feasible — but only if you cleanly separate both incomes and know the rules: Härteausgleich up to €820, a filing duty from €410 profit, the €24,500 trade-tax allowance, a Kleinunternehmer limit of €25,000, and a tax reserve of 30–40 %. Get that on autopilot from the start and the first tax assessment in April won't be a moment of dread.

Norman handles the operational finance work behind the scenes

From invoicing to bookkeeping, Norman keeps recurring finance work organized so you can stay on top of deadlines with less manual effort.