German Tax Registration Questionnaire (Fragebogen): A Step-by-Step Guide 2026

When you go self-employed in Germany, you must submit the tax registration questionnaire (Fragebogen zur steuerlichen Erfassung) via ELSTER. This guide walks you through the form section by section and explains the high-stakes fields.

- Category

- Founding

- Updated

- Author

- Diana

When you start self-employment in Germany — whether as a freelancer, sole trader, or GmbH managing director — you must register with your local tax office (Finanzamt). The instrument for this is the Fragebogen zur steuerlichen Erfassung (tax registration questionnaire). Getting it right determines your advance tax payments, VAT obligations, and profit calculation method — and helps you avoid overpaying or being estimated by the Finanzamt.

Key Facts at a Glance

- What: the official tax registration of your self-employment with the Finanzamt.

- Deadline: within one month of starting your activity (§ 138 AO).

- Where: electronically via ELSTER only — paper filing only in hardship cases.

- Result: the Finanzamt issues your Steuernummer (processing takes around 2–6 weeks).

- Highest-stakes fields: small-business exemption (§ 19 UStG) vs. standard VAT, accrual vs. cash VAT, VAT ID, and your expected profit (which drives your advance payments).

- Cost: none — the questionnaire itself is free.

What Is the Fragebogen zur steuerlichen Erfassung?

The tax registration questionnaire is the official form you submit to the Finanzamt. With it you open your tax file: the tax office learns what you do, how much you expect to earn, and which taxes apply to you. On that basis it sets your advance payments and assigns you a Steuernummer (tax number), which you then put on every invoice.

The form comes in several versions — scope and mandatory fields differ by legal structure:

| Legal structure | Version of the questionnaire | Notable feature |

|---|---|---|

| Freelancer, sole trader | Commercial / freelance (self-employed) activity | Standard form, around 8 substantive sections |

| GbR, OHG, KG | Partnership formation | Details of all partners, profit allocation |

| GmbH, UG, AG | Corporation formation | Articles of association, opening balance sheet, corporate tax |

This guide focuses on the most common version, for freelancers and sole traders.

Who Must Submit It — and By When?

Anyone starting self-employed activity is required to submit the form — freelancers, traders, and GmbH/UG founders alike. Even as a small business (Kleinunternehmer) you are not exempt.

The deadline is within one month of starting your activity (§ 138 AO). If you register a Gewerbe (trade), the Finanzamt is often prompted automatically — the trade office forwards your registration. Freelancers receive no automatic prompt and must submit the form proactively. File late and you risk a forced fine and an estimated tax assessment.

For help telling freelancer from trader status apart, see Freelancer or trader (Gewerbetreibender). The differences between your various German tax numbers are covered in Steuernummer, Steuer-ID and VAT ID.

The Questionnaire, Section by Section

ELSTER guides you through the form and automatically hides sections that don't apply. For sole traders, the questionnaire breaks down into these blocks:

| Section | What it asks | What to watch out for |

|---|---|---|

| Personal details | Name, date of birth, address, religion, tax ID | Must match your ID document exactly |

| Bank account & SEPA | Account for refunds, optional SEPA direct debit | Use a separate business account, not a mixed personal one |

| Tax advisor / authorized recipient | Who receives notices and mail from the Finanzamt | Only fill in if someone represents you |

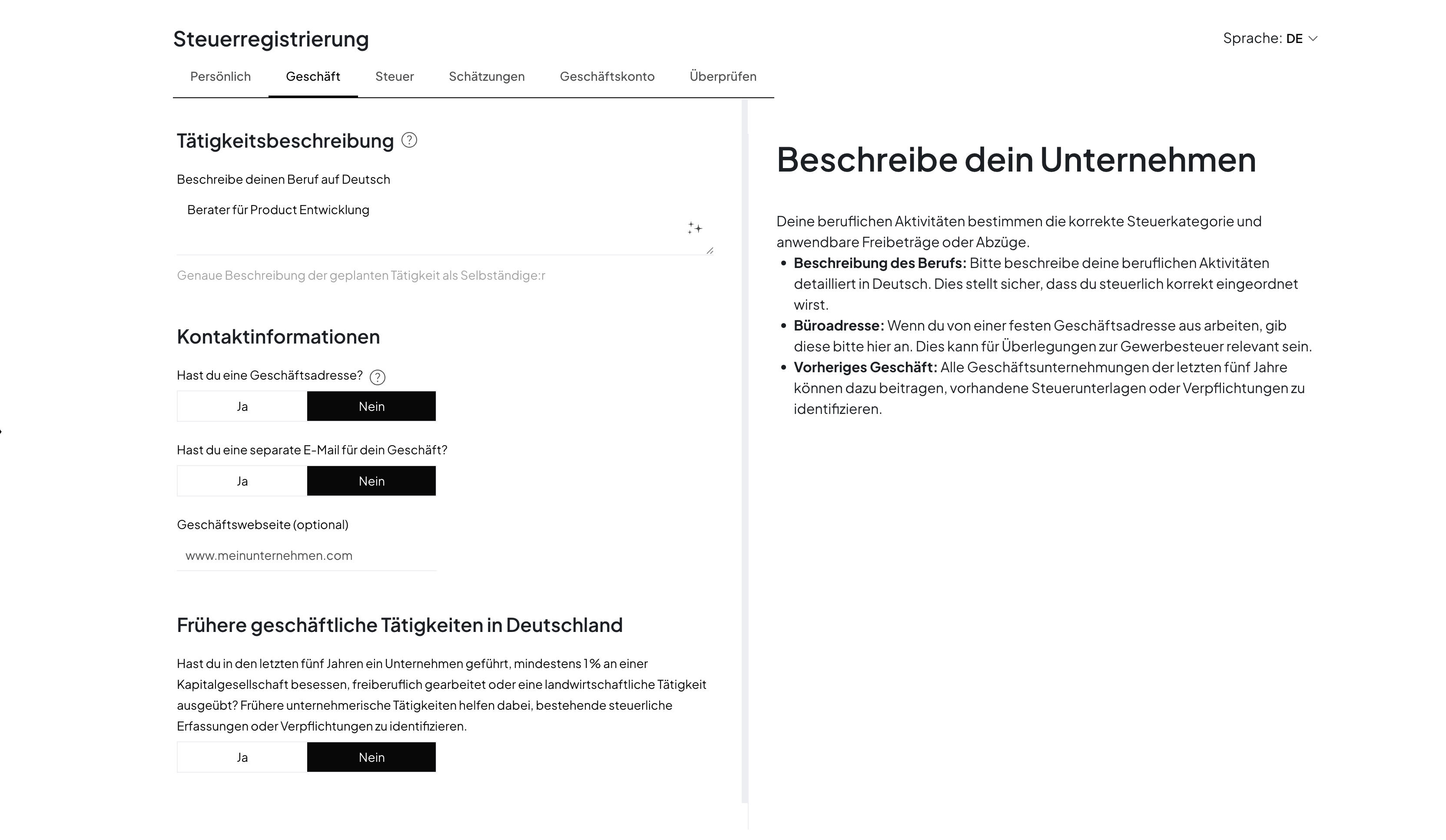

| Activity details | Type of activity, business name, start date, location | Determines freelancer (§ 18 EStG) vs. trade (§ 15 EStG) |

| Formation type | New founding, takeover, conversion; activity in last 5 years | For a takeover: details of the predecessor |

| Profit determination | Income-surplus accounting (EÜR) or full bookkeeping | Most founders choose the EÜR |

| Advance payments | Estimated profit in the founding and following year | Basis for income- and trade-tax advance payments |

| VAT | Small business (§ 19) or standard VAT, accrual/cash VAT, filing period | The most consequential page of the form |

| VAT identification number | Request a VAT ID for EU trade | Best requested at the same time |

| Payroll tax | Only relevant if you employ staff | Otherwise leave blank |

There are two fields that really matter in the Fragebogen: your business activity and your expected revenue for this year and next year. The first one indicates whether you're a Freiberufler or a Gewerbe. The second indicates whether you're a Kleinunternehmer or not.

Peter BoykoFounder of Norman

Peter BoykoFounder of NormanMost fields are quick to fill in. But three decisions have effects that last for years — let's look at those more closely.

The starter book for your self-employment

Free e-book: registration, accounting, your first invoice, and taxes — plus a tax calendar, deductions cheat sheet, and invoice template.

Small-Business Exemption or Standard VAT?

This is one of the most consequential decisions in the form. Under the small-business exemption (§ 19 UStG), you don't charge VAT on your invoices — this simplifies your bookkeeping considerably, you file no VAT returns, and you remit no VAT. In return, you also can't recover input VAT on your expenses.

You can use the exemption if your turnover in the founding year doesn't exceed €25,000 (threshold from 2025). In later years: prior-year turnover up to €25,000 and current-year turnover up to €100,000.

Standard VAT makes sense if you work mainly B2B and have significant input tax to recover — for software, equipment, or office rent, for example. Note: if you voluntarily waive the small-business exemption in the form, that choice binds you for five years.

For a detailed comparison with examples, see The Kleinunternehmer VAT exemption explained.

Accrual or Cash VAT (Soll- vs. Ist-Versteuerung)?

Here you decide when you remit VAT to the tax office:

- Soll-Versteuerung (accrual): VAT becomes due as soon as you issue the invoice — regardless of whether the customer has paid.

- Ist-Versteuerung (cash): VAT becomes due only once the customer pays.

For most founders, cash-basis VAT is more favourable, because you never have to front VAT you haven't received yet. You can elect it if your prior-year turnover is under €800,000 — which is practically always the case for founders. Tick the relevant box actively, otherwise you default to accrual VAT.

Request Your VAT ID at the Same Time

In the VAT section you can request a VAT identification number (USt-IdNr). It is not the same as your tax number: you need the VAT ID for trade with business partners elsewhere in the EU. Tick the box right here so you don't have to apply for it separately later. The distinction between your tax number, tax ID, and VAT ID is explained in Steuernummer, Steuer-ID and VAT ID.

Estimating Your Expected Profit Realistically

The Finanzamt uses your expected profit to set your advance tax payments. Overestimate and you pay too much upfront, tying up liquidity. Underestimate and you face a back-payment plus interest later — often together with simultaneously raised new advance payments. A realistic projection based on your planned income and costs is therefore essential.

Your estimated VAT liability also determines how often you file VAT returns (Umsatzsteuervoranmeldung):

| Expected VAT liability (prior year) | Filing period |

|---|---|

| over €7,500 | monthly |

| €1,000 to €7,500 | quarterly |

| up to €1,000 | annually (exemption possible) |

Good to know: the formerly mandatory monthly VAT return for new founders is suspended from 2021 through 2026 inclusive. You'll generally start out filing quarterly, as long as your estimated liability stays below €7,500.

How to Submit the Form

You have two routes for submitting the questionnaire.

With Norman — guided and free. Norman is one of the largest registration services for the self-employed in Germany, and has rebuilt the questionnaire so you fill it in in plain language — without the ELSTER jargon. You answer clear questions about your activity, your estimates, and your bank account; Norman maps them to the correct fields and submits the form for you — free of charge.

Manually via ELSTER. You can also fill in the questionnaire directly in the ELSTER portal — since 2021, electronic submission is mandatory:

- Create an ELSTER account — activation can take up to two weeks, as the activation code arrives by post.

- Under "Formulare & Leistungen" → "Alle Formulare" → "Fragebogen zur steuerlichen Erfassung", choose the right version.

- Complete the form carefully — ELSTER hides sections that don't apply.

- Submit electronically and wait for your Steuernummer to be assigned (around 2–6 weeks).

Common Mistakes to Avoid

- Wrong activity classification: Check whether you're a Freiberufler or Gewerbetreibender before submitting — it has significant tax consequences.

- Unrealistic profit estimate: Too low triggers back-payments; too high means overpaying advance tax.

- Rushing the VAT choice: Voluntarily waiving the small-business exemption binds you for five years.

- Personal instead of business account: A mixed account complicates bookkeeping and gives the Finanzamt visibility into your private transactions.

- Submitting late: After one month, you risk a forced fine and an estimated tax base.

Frequently Asked Questions

How much does the tax registration questionnaire cost?

Nothing. Registering with the Finanzamt via ELSTER is free. Costs only arise if you have a tax advisor help you.

Do I need a tax advisor to fill it in?

No. You can complete the questionnaire yourself — ELSTER guides you through the fields. For more complex cases (e.g. founding as a team or an unclear activity classification), advice can be worthwhile.

How long until I receive my tax number?

Usually 2 to 6 weeks after submission. File early — without a tax number you can't issue proper invoices.

Do I have to submit it even as a small business (Kleinunternehmer)?

Yes. The small-business exemption only frees you from charging VAT, not from registering for tax. Every self-employed person must submit the form.

What happens if I submit it late?

The Finanzamt can impose a forced fine and estimate your tax base. Both are avoided by meeting the one-month deadline.

Conclusion

The tax registration questionnaire is the first and most important administrative step for anyone going self-employed in Germany. Getting it right — especially the VAT choice and the profit estimate — sets up your tax obligations correctly from day one. Norman helps you track your income, expenses, and tax obligations from the moment you're registered — without needing a tax advisor for day-to-day bookkeeping.

Norman handles the operational finance work behind the scenes

From invoicing to bookkeeping, Norman keeps recurring finance work organized so you can stay on top of deadlines with less manual effort.